By Advocata Institute

The recent imposition of tariffs on trade by the United States on Sri Lankan exports is a wake-up call. While concerns about the bilateral US-Sri Lanka trade imbalance have been noted, a close reading of the Office of the US Trade Representative’s (USTR) findings suggests deeper grievances—rooted not only in tariffs, but in the wide array of non-tariff barriers and para-tariffs Sri Lanka continues to maintain.

Sri Lanka’s protectionist trade regime—characterised by ad hoc levies, price controls, import quotas, midnight gazettes and opaque customs practices—has long been a source of concern for trading partners. Many of these measures lie outside the WTO framework, creating both inefficiencies and unpredictability in the trading environment.

This moment should be seen not merely as a diplomatic challenge, but as a strategic opportunity to initiate and accelerate long-overdue trade reform. Rationalising our tariff structure, rapidly phasing out para-tariffs, addressing behind-the-border barriers, and improving trade facilitation will not only help rebuild trust with key partners like the US, but also improve Sri Lanka’s overall competitiveness and resilience as well as the appreciation of gains on trade.

Trade policy must now move beyond protectionism and towards enabling integration into global value chains. The cost of inaction will be borne by Sri Lankan exporters, consumers, and our broader growth ambitions.

While tariff rationalisation and the removal of non-tariff barriers are urgent priorities, they are only the first steps toward a broader, more strategic reset of Sri Lanka’s trade and competitiveness agenda.

Global trade patterns are shifting rapidly, shaped by geopolitical rivalry, supply chain realignments, and the revival of regional trade agreements. From the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) to the Regional Comprehensive Economic Partnership (RCEP), countries are moving decisively to lock in market access, deepen integration, and improve resilience. Sri Lanka, however, risks being left behind.

Sri Lanka must now actively consider accession to regional trade blocs and seek bilateral agreements with both traditional and emerging partners. Improving trade facilitation, digital trade readiness, and regulatory coherence will further boost productivity and investor confidence

India and Sri Lanka share a unique and evolving economic relationship rooted in geography, history, and culture. With India projected to become the world’s third-largest economy by 2030 and Sri Lanka seeking to stabilise and grow post-crisis, deepening bilateral economic integration offers mutual benefits. The Indo-Sri Lanka Free Trade Agreement (FTA), in force since 2000, provides a strong foundation, enabling over 60% of Sri Lankan exports to benefit from preferential access. However, Sri Lanka has not fully realised the benefits of this agreement. Due to non-tariff barriers (NTBs), complex rules of origin, and tariff quotas on key export items—such as tea and garments—have constrained trade. Moreover, Sri Lankan manufacturers have struggled to integrate into Indian supply chains due to limited industrial alignment and technical bottlenecks. These are not reasons to abandon the agreement, but rather imperatives to improve it.

It is time to revive and conclude the Comprehensive Economic Partnership Agreement (CEPA) with India—a framework negotiated over 13 rounds and nearly finalised in 2008. CEPA aims to go beyond goods to cover services, investments, and regulatory cooperation. If well-designed and transparently negotiated, it could address many of the constraints holding back Sri Lankan exporters, support investment inflows, and enable service-sector expansion—particularly in IT, logistics, and education.

Gain from greater integration

Sri Lanka can gain from greater integration, especially by tapping into India’s expanding middle-class—expected to reach 700 million by 2030—and attracting Indian investment into tradable sectors. Investment in ports, energy, IT, and hospitality can enhance Sri Lanka’s competitiveness, job creation, and foreign exchange earnings. Colombo and Trincomalee ports, grid connectivity for affordable power, and service sector integration—particularly in IT, aligned with Sri Lanka’s ambition to grow its tech workforce—are promising avenues.

Sri Lanka’s path to deeper integration must also address domestic constraints: a narrow export base, protectionist policies, and ageing demographics. However, with targeted reforms and investment, Sri Lanka can participate in India’s supply chains through niche products and intra-industry trade, rather than competing head-on. Indian firms investing in Sri Lanka can re-export to India, leveraging their networks while transferring skills and technology locally.

Policymakers can institutionalise collaboration through a bilateral Economic Cooperation Council or joint task force focused on trade, investment, and regulatory alignment. Regular exchanges among academics, think tanks, and officials can help adapt successful Indian policy lessons to Sri Lanka’s context—paving the way for shared growth and regional stability.

Globally, countries are deepening ties to protect against trade shocks and seize new markets. The EU has accelerated negotiations with ASEAN states and Mercosur; Canada is expanding its trade footprint across Asia; and blocs like the CPTPP and RCEP are fostering tighter regional integration. If Sri Lanka remains on the sidelines, it risks being left out of emerging trade frameworks that will define global commerce over the next decade.

Deepening trade ties with India is not without challenges. But the alternative—continued stagnation and vulnerability to arbitrary tariffs or shifting investor sentiment—is far worse. Sri Lanka must move beyond domestic hesitation and re-engage India in good faith. A renewed CEPA—anchored in mutual benefit, transparency, and safeguards for sensitive sectors—can serve as a cornerstone of a modern, outward-oriented economic strategy.

We urge the Government of Sri Lanka to seize this opportunity—push for the implementation of CEPA, invest in domestic capacity to meet quality standards, and remove barriers that hold our firms back from regional value chains. If we act decisively, Sri Lanka can transform a once-contentious FTA into a platform for inclusive growth and sustained global relevance.

The Advocata Institute strongly urges the Sri Lankan Government to eliminate para-tariffs such as CESS and the Ports and Airports Levy (PAL), which have long hindered Sri Lanka’s trade competitiveness. These additional taxes that sit on top of general import duties increase costs for businesses making it expensive for inputs for manufacturing, disincentives entrepreneurs in taking risks in the global market ultimately making Sri Lankan exports less competitive in global markets. These tariffs also make day to day items expensive for the average Sri Lankan to serve a narrow interest of people. Removing para-tariffs and accelerating the current program of tariff reform to be more uniform would not only cushion the impact of US tariffs but also enhance Sri Lanka’s overall economic resilience.

US trade tariff policy

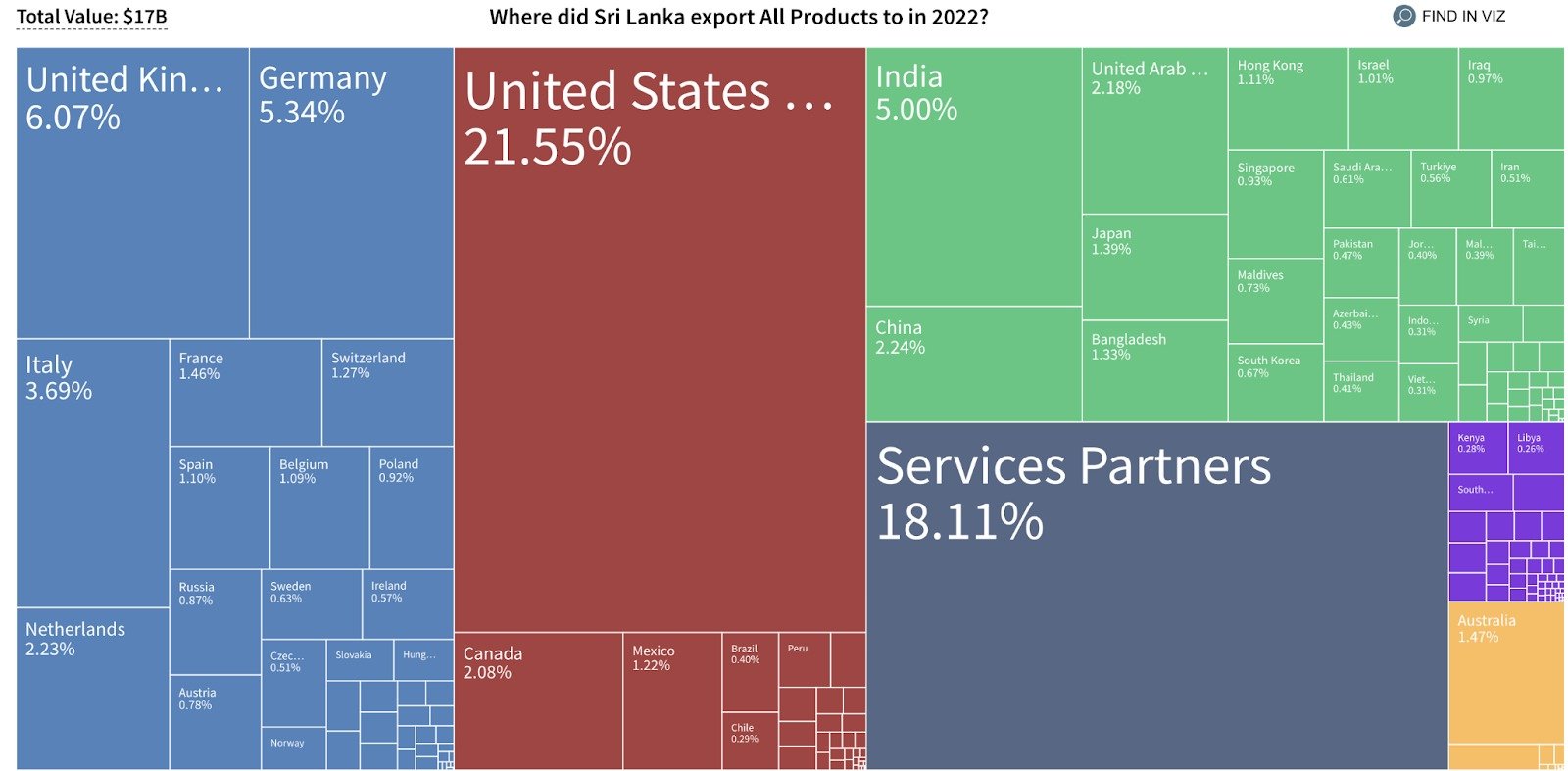

There is growing concern over the US government’s proposed tariff hikes, particularly the 44% tariff on Sri Lanka. These tariffs, part of a broader 10% universal duty on all imports, threaten to disrupt trade relationships, impact key industries such as the apparel sector, and exacerbate economic challenges for developing economies reliant on US markets. The new trade measures by the Trump administration include a universal 10% tariff on all imported goods, effective April 5, and additional “reciprocal tariffs” targeting specific countries with which the US has significant trade deficits, set to begin 9 April. Sri Lanka is set to be hit with a 44% tariff. The US is Sri Lanka’s largest export destination, accounting for approximately 23% of total merchandise exports in 2024, with apparel making up over 70% of these exports. The new tariff threatens the competitiveness of Sri Lankan garments in the US market, potentially leading to reduced orders.

Trump’s trade policy is largely driven by domestic political pressures, and his desire to tap into populist sentiments of his electoral coalition, positioning himself to be the protector of American industry and Jobs. Another driver of the policy is the US strategic competition with China and the Trump administration’s desire to use tariffs as a blunt diplomatic instrument to assert its influence in a fractured world.

These policies are however based on flawed economics. The notion that imposing tariffs will “balance” trade deficits between countries is rooted in outdated mercantilist thinking. Just as businesses and families buy goods and services from some people and sell their labour and products to others, so do countries. The idea that trade has to be balanced between two countries is as flawed as thinking that just because we buy our groceries from the supermarket we must also sell to them in order to benefit from the transaction.

Illogical as they are, Trump policies expose the protectionist policies of Sri Lanka, and the country’s lack of export diversification and lack of integration into regional value chains.

Sri Lanka’s protectionism

For nearly 20 years, Sri Lanka has been engaging in a similar protectionist policy regime. Protecting domestic industrialists at the cost of the competitiveness of the overall economy.

With Sri Lanka facing a 44% tariff, the country’s apparel and textile sector—one of its largest export industries—will suffer significant losses. Given Sri Lanka’s dependence on US demand, these trade measures, could lead to:

Reduced competitiveness in key export industries.

Global supply chain disruptions as buyers shift to countries with lower tariffs.

Declines in investment and employment, further straining an already fragile economy.

Similar consequences will be felt in Vietnam, Bangladesh, Cambodia, and Myanmar, where heavy tariffs will challenge their economic stability. The entire South Asian region faces risks of declining foreign investment and trade uncertainty, further slowing economic recovery efforts.

Sri Lanka’s dependence on a few export markets is a direct result of pursuing a failed import substitution policy in the guise of ‘industrial policy’ that has caused corruption, political dysfunction and incentives domestic entrepreneurs and capital to produce for the domestic market in order ‘to save dollars’. Ironically, the logic that has shaped Sri Lanka’s trade policy is similar to the one pursued by Trump.

Advocata Institute recommendations

To strengthen Sri Lanka trade competitiveness and mitigate the impact of US tariffs, Advocata Institute recommends the following policy actions:

Eliminate all para-tariffs on imports signalling Sri Lanka’s openness to trade with the world.

Negotiate with the US on tariff levels with US imports with US tariff levels to promote fairer trade conditions.

Accelerate the program to move towards a more uniform and a simplified tariff facilitating trade and eliminating room for corruption.