By Dhananath Fernando

Originally appeared on the Morning

US President Donald Trump’s second term seems to be keeping all people around the world on their toes. The changes and policies, along with their implications, will be complicated, and we have to do our homework to gain an advantage or at least survive in this game.

The new Trump administration has suggested reciprocal tariffs, meaning the same tariff rates applied to each country that they charge for US products.

Already, a 10% tariff is in effect for non-energy products from Canada and a 25% tariff on energy-related products from Canada. Additionally, a 25% tariff has been imposed on Mexican products, alongside an additional 10% tariff on Chinese products, bringing the total tariff on Chinese products to 21% (from around 11% previously).

SL’s opportunities and challenges

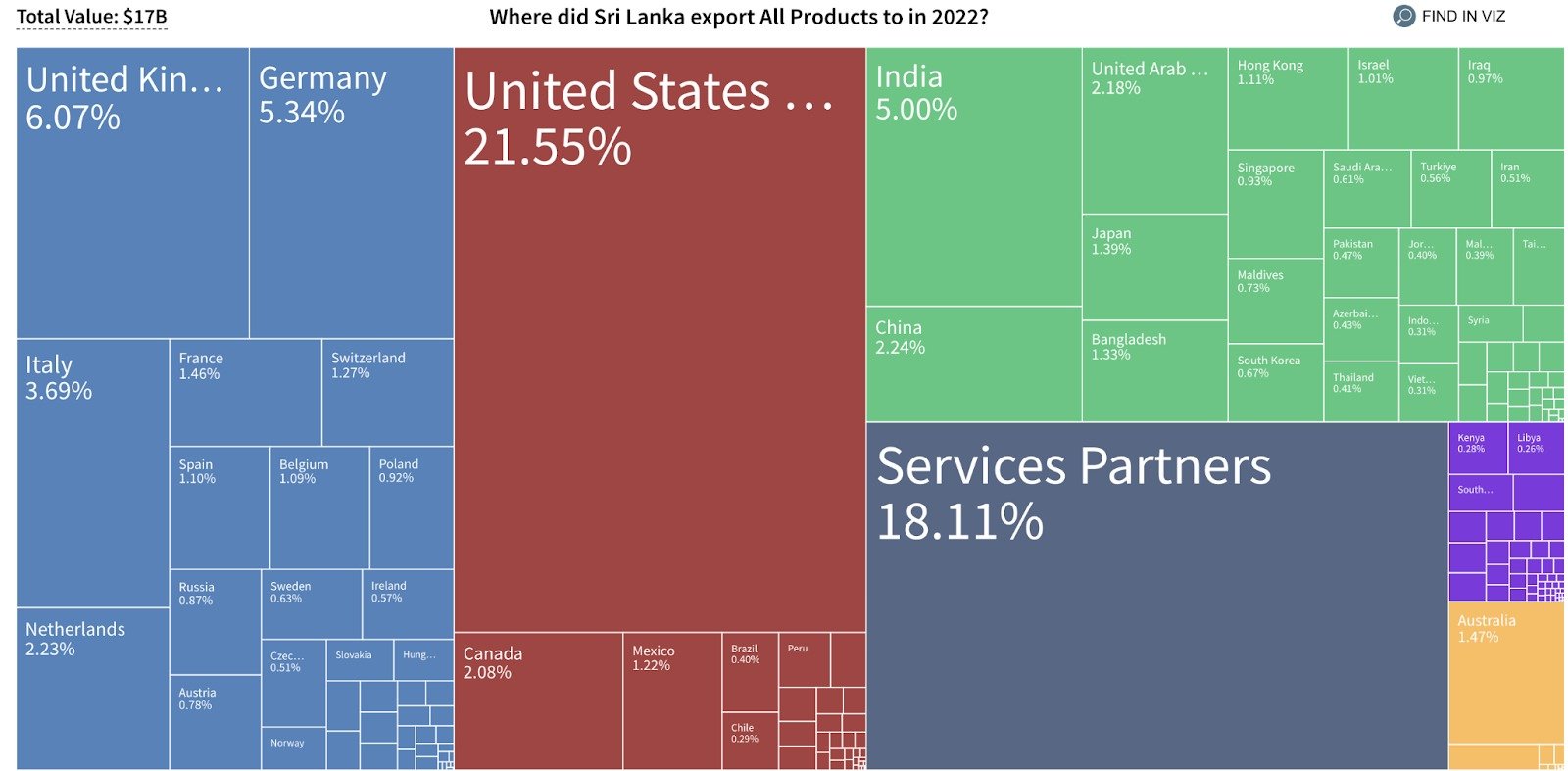

Before Sri Lanka gets affected by any reciprocal tariff, we first need to understand our total exports, including services.

According to Harvard’s Atlas of Economic Complexity, we export about 21% to the United States. When it comes to apparel, about 40% of our apparel exports are destined for the US.

Accordingly, the first line of impact for Sri Lanka would be potential consumption contraction in the US. With high tariffs even against Canada, China, and Mexico, as well as increased prices of essential products, the US consumer will likely reduce spending on non-essential items such as seasonal clothing. It is normal consumer behaviour to postpone purchasing decisions if expenditure on essentials like energy and rent increases.

The second line of impact has both positives and negatives. China and Mexico also supply apparel to the US. If relative prices of Sri Lankan apparel become lower following the 25% tariff for Mexico, we might gain an advantage.

Similarly, we could become more competitive than China, which now faces an overall 21% tariff. Therefore, we must be cautious and prepared, recognising it is not just tariffs on Sri Lanka directly but also tariffs on others that can bring us opportunities or challenges.

The danger lies in the final stage if the US imposes reciprocal tariffs. The US would consider imposing the same tariffs for Harmonised System (HS) codes as the other trading country imposes on US products.

There is discussion that the US might not only consider customs duties but also other tariff barriers and even non-tariff barriers. In that case, Port and Aviation Levy (PAL), Commodity Export Subsidy Scheme (CESS), Social Security Contribution Levy (SSCL), and Value-Added Tax (VAT) might be considered, according to some reports.

This decision depends entirely on the Office of the US Trade Representative (USTR) defining ‘unfair trade practices.’ Media reports indicate that the USTR is expected to analyse all data and make a decision on reciprocal tariffs by 1 April.

We must recognise that Sri Lanka’s average tariff rates are significantly higher than those proposed by the US to China, Mexico, and Canada. A 25% tariff in Sri Lanka is considered low, as our effective tariff rates reach nearly 100%, and for vehicles with excise duties, it exceeds 200%. It is joked that even Trump would become confused if he learnt about Sri Lanka’s tariff structures and that he might learn a tough lesson from us.

In the context of reciprocal tariffs, price-sensitive product categories such as food, apparel, and rubber products may face higher prices in US markets. Ultimately, the real impact will depend on how other competing export markets are affected by US tariffs and non-tariff barriers and how these affect US consumption and global economic growth under new trade dynamics.

Meanwhile, Europe and other powerful countries are targeting the US with reciprocal tariffs, which could trigger global supply chains to consider relocation and create new incentive structures. This can present either an opportunity or a disaster for Sri Lanka.

Solutions

To attract new supply chains and assembly components, we must quickly work on basic factor market reforms. Having adequate land ready for industry and a flexible labour force with business consciousness is essential. Secondly, simplifying and lowering our tariff structure is critical, even though it might be somewhat late.

Additionally, exploring exports towards East Asia and the Indian market is increasingly vital. Whether our US market shrinks or not, we should prepare to explore other markets, primarily India and East Asian countries. Strengthening foreign relationships, activating business chambers, and intensifying diplomatic missions to strengthen ties is necessary.

Accelerating regional free trade agreements and conducting market sentiment research can help Sri Lankan entrepreneurs expand their exports. Fundamentally, economics never expires – even during trade wars or crises, strong economic fundamentals provide the best way to survive and thrive. We must move from hope to action.

Where did Sri Lanka export all products to in 2022?

Source: Harvard Atlas of Economic Complexity

Where did Sri Lanka export textiles to in 2022?

Source: Harvard Atlas of Economic Complexity