Originally appeared on The Morning.

By Dhananath Fernando

I travel mainly by a common staff transport from Moratuwa to Colombo to work. I travel by train as well as on normal public transport for other travel purposes. Undoubtedly, my staff transport is the most efficient and affordable, providing the most value for money. It not only provides value for the money I pay, but it also provides a great example of why the Government should not do business and why the private sector should be allowed to. Even in the toughest conditions, private enterprises can bring solutions.

The operator of my private staff transport is Amal, an executive at an office in Colombo. While a normal bus typically has three main stakeholders, Amal has made it so that there’s just one main stakeholder. That’s efficiency. A normal bus on the road generally has an owner, a driver, and a conductor. Amal just has one. He is the driver who drives us all safely and on time. He does not have a conductor because he has an automated door which the driver can operate easily with just a switch in the dashboard.

He charges about Rs. 12,600 for an air-conditioned bus ride for the entire month. That is approximately Rs. 286 per one-way journey from where I live, which is around 20 km. If I were to calculate my cost per kilometre for a peaceful air-conditioned bus ride where I can sleep comfortably or work on my computer, it costs just Rs. 14.

Even if I travel by a normal non-air-conditioned bus, the incremental value I pay for Amal is negligible. If I use an air-conditioned bus, my costs are higher than what Amal charges. In the first place, there are no air-conditioned buses where I live and with Amal, my travel time is almost one-third of the total time taken on the normal route. I believe that travelling with Amal not only saves time but also reduces carbon emissions as well.

A win-win situation

Amal is just one man in the private sector who adds value to my life while making a profit and a living out of it. He recently bought another bus and now he has two rosters both ways with a time gap of about 30 minutes, meaning I can choose either the first bus or the second according to my convenience. He shares the live location on WhatsApp before every ride, so I can track where the bus is and be prepared.

Amal is not the only such person. If you observe Colombo between 7-9 a.m. you will notice that there are many buses operating on the same model as Amal’s. There is no regulatory authority on staff transports in Colombo and yet it operates efficiently, with both Amal and I being beneficiaries of the system. It’s a complete win-win. I hope that after reading this article, there won’t be any Government regulations set up regarding staff transport to ruin the market.

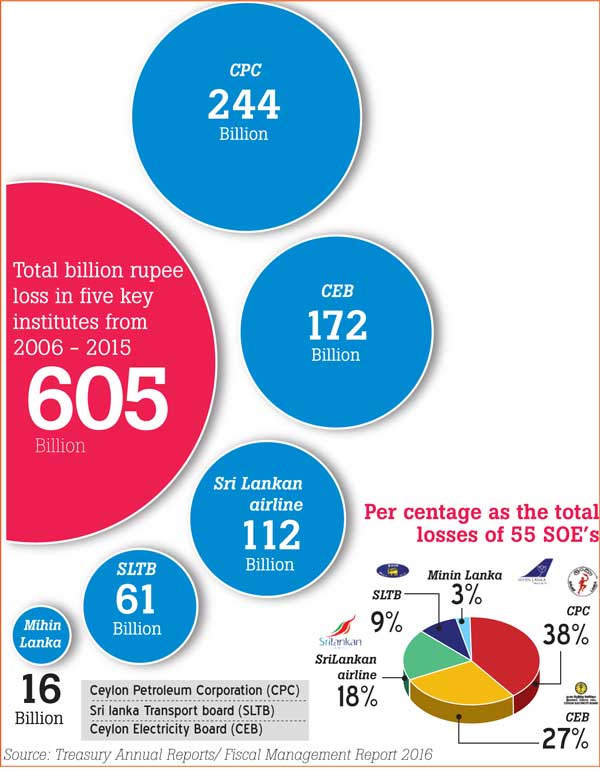

Amal is a one-man private operator who solves a burning issue for me or at least provides me with a reasonable solution which my Government has been unable to provide for more than three decades, even with billions worth of funds.

Amal can improve efficiency because he has an incentive for improving efficiency. His incentive has a ripple effect leading up to minimising carbon emissions.

Privatisation to solve problems

Given the discussion on privatisation, there is no better example than Amal of how private enterprises help people. Economics and businesses are all about solving people’s problems. Our life is all about solving each other’s problems and depending on each other. Amal solves my transport problem and by paying him, I may be contributing money for his child’s education.

Our entire economy is a complicated yet interconnected web. Efficiency and getting the maximum out of our resources are needed, which can only be done when the markets are in operation. Markets are operated by private individuals like you and me who read this article.

While the process of privatisation is complicated, privatisation is just a normal process for market operations. Sri Lanka’s economic problem is that we don’t solve anybody’s problems. When we do not solve problems, how can we earn money? How can others solve our problems?

Problem-solving is nothing but improving efficiency. Efficiency can only be improved when people have incentives. It is a universal truth, like the earth revolving around the sun. Even if you look at the Return on Equity (ROE) or Return on Assets (ROA), which are indications of a company’s efficiency, it is very clear that under normal circumstances and on level playing fields, the private sector’s efficiency and impact is much higher than when the Government runs businesses.

Just take a look at Figure 1, which is a comparison between Sri Lanka Telecom (SLT), which has some private sector engagement and Dialog, which is a private sector player.

Figure 1: ROE analysis of SLT vs. Dialog

Source: Annual Reports of SLT and Dialog (2018-2021)

In some cases, the State sector ROE is simply higher because of the absence of a level playing field. The banking sector is a good example. Most State banks get preferential treatment so their returns are high due to the non-competitive nature of getting businesses. Given the size of the Government, most Government banking is done through the State-owned People’s Bank and Bank of Ceylon. Anyone visiting a State bank and a private bank will experience the difference in service levels. This doesn’t mean the private sector is perfect; markets are always imperfect, but it is obviously many miles ahead of businesses run by the State.

Figure 2: ROE comparison of the banking sector

Source: State of the State-Owned Enterprises, Advocata Institute (2022)

The private sector is not anyone else, it is us. We should be given the opportunity to solve our problems instead of making the Government solve them. When the Government tries to solve the problem, it will not only block the private sector but it will also waste our tax money. Just think of Amal; he is providing me with a reasonable solution to a problem that the Government has been unable to solve for over three decades.

The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute or anyone affiliated with the institute.